AnryMos

Introduction

Microsoft (NASDAQ: MSFT) is widely considered a safe-haven, bond-type investment due to its incredible trading moat, solid financial performance, strong balance sheet, and colossal capital return program. However, Microsoft lost around 25% of its market capitalization in 2022 as Treasury yields jumped due to monetary tightening. Politics. In today’s note, I’m running Microsoft through my quantitative analysis process and my TQI rating model to see if it’s undervalued or overvalued and to determine if it’s a a good long-term buy at current levels.

Although we’re focusing on the numbers and charts in this note (and not the company itself), you can find my perspective on Microsoft’s business and my investment thesis through my past coverage of the Microsoft business. company (newest first):

Before constructing an absolute valuation for Microsoft, let’s quickly analyze Microsoft’s fundamental, quantitative, and technical data.

Looking at Microsoft through the lens of TQI’s quantum analytics process

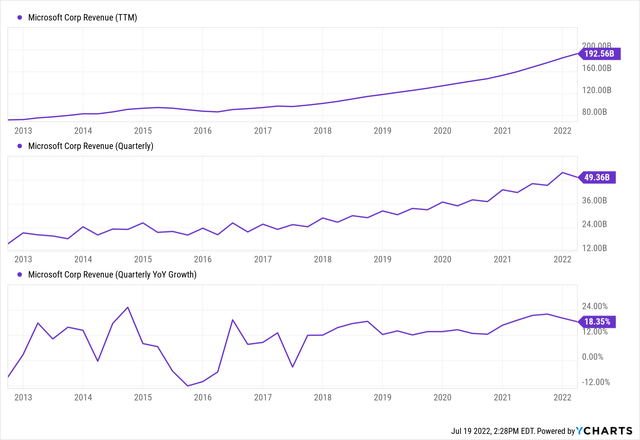

In the digital age, technology is ubiquitous, and Microsoft has built incredible business moats across its huge addressable and usable markets, including cloud, enterprise software, games, and more. Over the past twelve months, Microsoft has raked in revenue of $192.5 billion, with first-quarter growth coming in at a healthy 18% y/y. Leverage the strength of its cloud infrastructure business [in addition to other solid growth in other business lines]Microsoft’s financial performance has been steadily strengthening for several years now.

Y-Charts

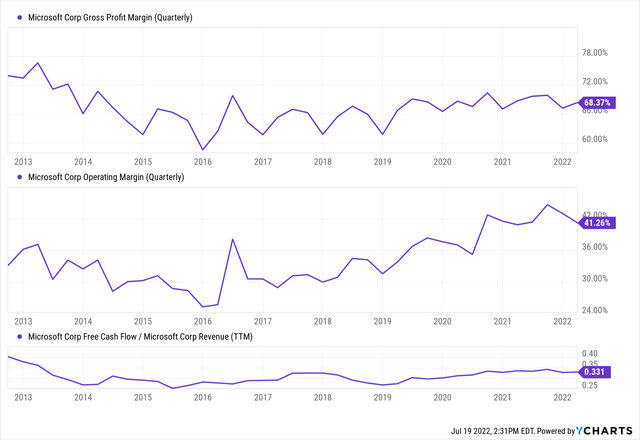

In addition to robust revenue growth, Microsoft’s margin profile is getting stronger with each passing quarter. For the first quarter of 2022, Microsoft reported gross and operating margins of 68% and 41%, respectively. As you may know, these are best-in-class numbers.

Y-Charts

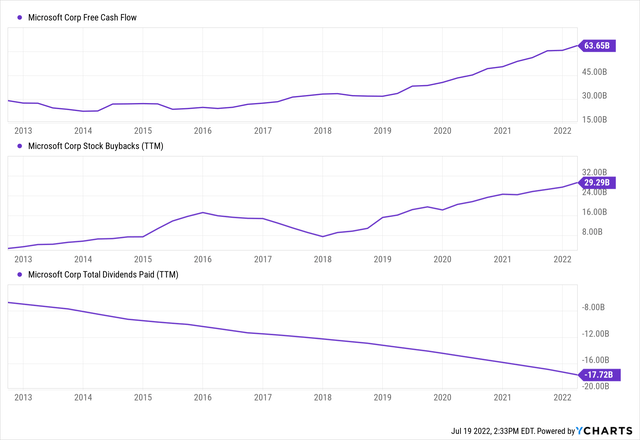

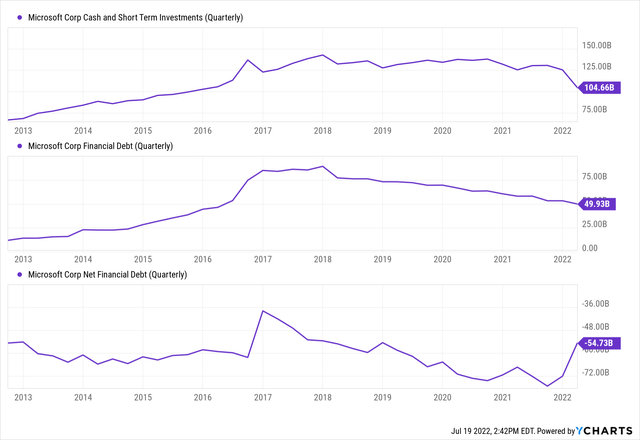

While recording healthy growth numbers at this massive scale, Microsoft also generates incredible steady-state FCF TTM margins of around 33%. It’s fair to say that Microsoft is a money-printing machine. In the last twelve months alone, Microsoft generated free cash flow of $63.65 billion. Due to a net cash balance of approximately $55 billion (cash), Microsoft’s management has adopted an aggressive capital return program, which constitutes massive stock buybacks and a healthy dividend.

Y-Charts

Y-Charts

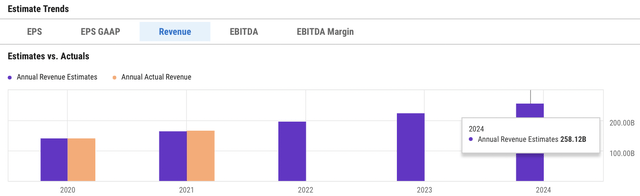

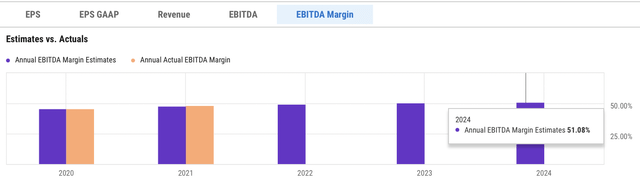

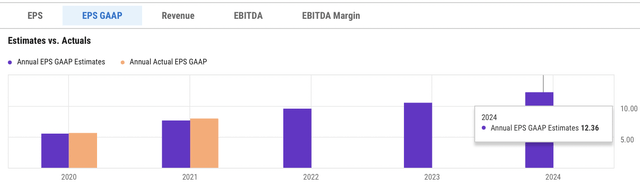

The threat of a global recession is growing; however, Microsoft may continue to generate sales and earnings growth in coming years (albeit at a slower pace). According to consensus estimates from YCharts analysts, Microsoft’s revenue is expected to grow from $198 billion in 2022 to $258 billion by 2024 at a compound annual growth rate of approximately 14%. During this period, Microsoft [EBITDA] margins are expected to improve by approximately another 200 basis points and expected earnings are expected to outpace expected revenue growth.

Y-Charts

Y-Charts

Y-Charts

While the fundamental outlook for Microsoft’s business looks rosy at the moment, things could change quickly if we find ourselves in a deep economic recession (as the FED raises interest rates and implements QT to reduce the inflation by lowering aggregate demand). According to recent reports, Microsoft is slowing hiring amid economic uncertainty (and has also cut some jobs in recent days). In my opinion, this news is proof that Microsoft’s business is not immune to the economic downturn. At this point, I don’t believe Microsoft’s financial projections will be achieved in a recessionary environment. Over the next several quarters, we may see a weakening of the company’s fundamentals.

Now, let’s shift gears and analyze some quantitative factor ratings for Microsoft.

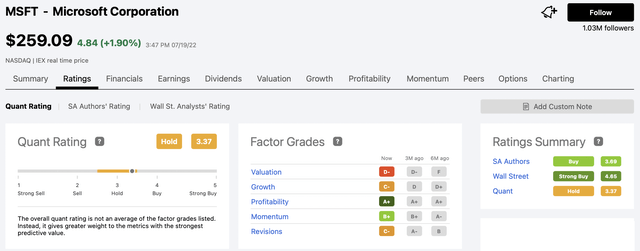

According to SA’s Quant rating system, Microsoft is classified as “Hold”; however, SA Authors and Wall Street analysts remain bullish on the counter. While Microsoft has maintained an “A+” rating on profitability, growth, revisions [earnings], and Momentum ratings have deteriorated over the past six months. Moreover, Microsoft’s improved valuation rating is only the result of negative price action. Overall, a Cumulative Quantitative Factor rating of 3.37/5 puts Microsoft firmly in “Hold” territory.

SA Quantitative Rating

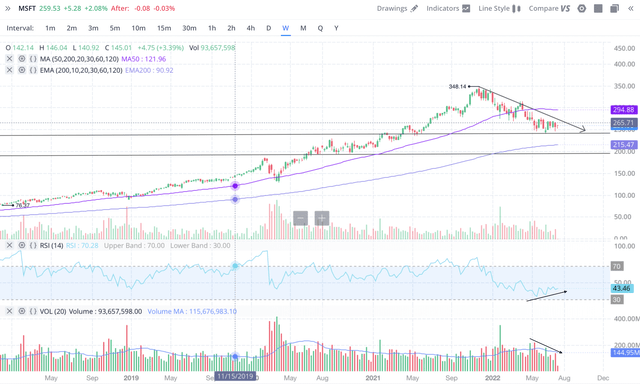

Since the Fed pivot in November 2021, Microsoft stock has slid lower in a downward wedge pattern. As you can see below, Microsoft is currently trading well below its 50-day moving average, a level it has exceeded during its bull run over the past few years.

webull

After falling around 25% in 2022, Microsoft stock appears to be forming a base on the weekly chart, with an increasing RSI. Additionally, volumes tended to decline, which could be seen as a sign of seller exhaustion. Technically, Microsoft seems ripe for a short-term rebound. However, the downtrend that started in late 2021 is still intact and based on valuations, Microsoft shares could see more downside in the medium term. Speaking of valuations, let’s now try to determine Microsoft’s absolute intrinsic value.

Finding Microsoft’s Fair Value and Expected Return

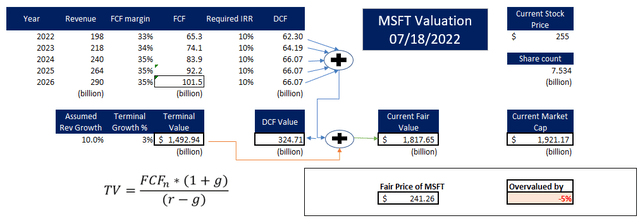

To find Microsoft’s fair value and expected return, we will use TQI’s valuation model with the following assumptions:

| 2022E revenue (conservative estimate) | $198 billion |

| 4.5-year forward revenue growth rate (%) | ten% |

| Terminal growth rate (%) | 3% |

| Optimized FCF margin (%) | 33-35% |

| Discount rate / IRR required (%) | ten% |

| Multiple output [P/FCF] | 15-25x |

Results:

TQI assessment model (tqig.org)

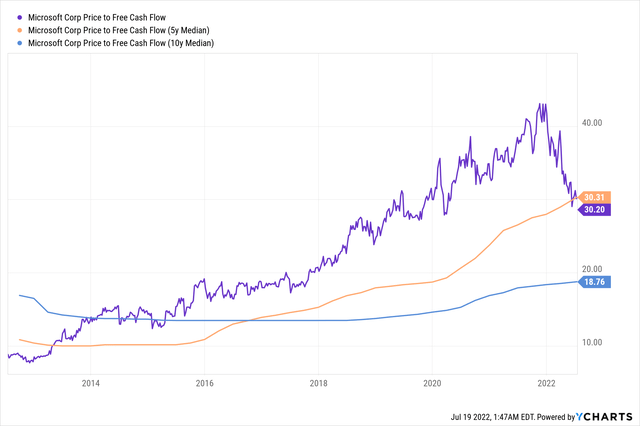

Despite using a lower discount rate (10%) than the IRR required by TQI for GARP stocks (15%), the Microsoft stock turns out to be slightly overvalued. The moderation in the valuation of the Microsoft stock brought its P/FCF multiple back to its median P/FCF over 5 years. However, there is more downside and no real upside for Microsoft’s trading multiples.

Y-Charts

In one of my previous articles, I described the logic behind Microsoft’s valuation moderation and, frankly, the recent surge in Treasury yields warrants further moderation in Microsoft’s trading multiples. As the economy potentially heads into a recession, Mr. Market is irrationally pricing Microsoft as a risk-free asset. While I think Microsoft is one of the strongest companies on this planet, it’s not immune to a recession (and Morgan Stanley seems to agree with my view, according to this report ).

Y-Charts

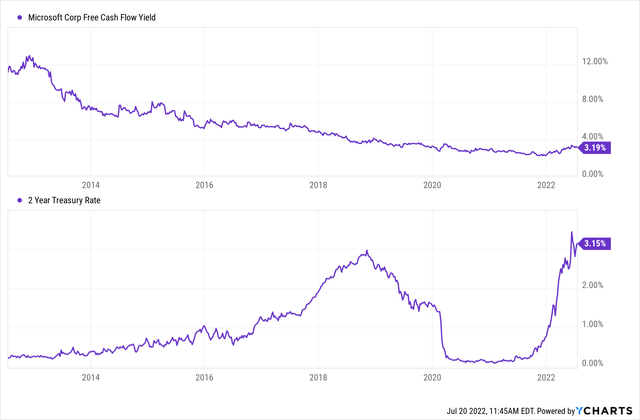

Why would someone buy Microsoft at an FCF yield of 3.21% when the 2-year Treasury yields 3.15%? (and that too in the face of an impending recession)

Well, I don’t have a good answer to that question, but let’s take a look at Microsoft’s expected returns to see what an investor could realistically make from here with Microsoft.

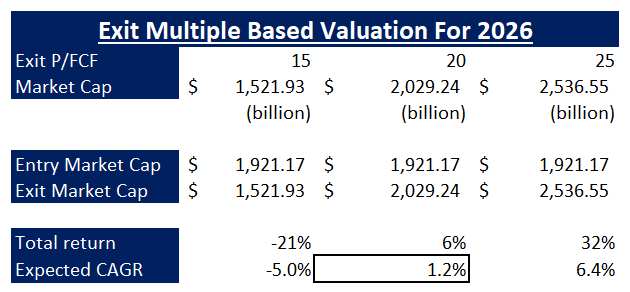

TQI assessment model (tqig.org)

Assuming a P/FCF multiple of approximately 20x in 2026 (inverse of 5% long-term average interest rates), Microsoft would only generate a price return of 6% from current levels over the next 4 , next 5 years. Therefore, Microsoft shares look like dead money to me. So far, we haven’t included Microsoft’s return on capital program in our analysis, and now is a good time to do so.

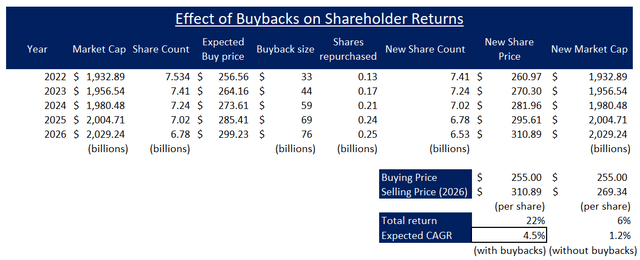

As you may know, Microsoft has a lot of cash on its balance sheet and generates tons of free cash flow every quarter. In recent years, Microsoft has implemented an aggressive return on capital program that includes dividends and stock buybacks. While we’ve discussed this program (and its potential) in detail in the past (report), I believe that if Microsoft’s $68.7 billion deal to buy Activision Blizzard (ATVI) goes ahead, the buyback program will be a bit smaller than my original estimate. Here’s what I expect from Microsoft’s buyout program over the next 4.5 years:

TQI assessment model (tqig.org)

After taking into account the effect of potential buyouts, Microsoft’s expected CAGR returns increased from 1.2% to 4.5%. With Microsoft’s dividend yield of

Final Thoughts

Even after a significant decline in 2022, Microsoft continues to trade at a premium valuation. The spread between Microsoft’s FCF yield and the 2-year Treasury has narrowed to just 0.06%, meaning the market is effectively viewing Microsoft as a risk-free security. While I understand that a high quality company like Microsoft deserves a higher valuation, I can’t stomach the fact that it’s rated as a risk-free asset. Microsoft’s business is not immune to recession (and economic downturns), period.

To determine Microsoft’s fair value, I lowered my discount rate to 10% (taking into account better business quality and treating Microsoft like a DGI game), and I still find it overvalued at current levels. From there, Microsoft’s expected CAGR return through 2027 is around 4.5% (including redemptions) and around 1.2% (without redemptions). Given that my base case is built with 10% annualized revenue growth and steady margin expansion, I wouldn’t call this assessment conservative. Therefore, I don’t like Microsoft’s $255 as a GARP or DGI game. Mr. Market continues to view Microsoft as a sound investment; however, a mid-reversion alone could lead to another 25-30% loss in stock. Plus, if we see a deep earnings downturn, Microsoft could face even more downside. Given the downside risk and little upside potential from current levels, I consider Microsoft to be neutral at current levels.

Takeaway key: I rate Microsoft neutral at current levels due to an unfavorable risk/reward profile.

Stewardship note: I will soon be launching a Marketplace service on Seeking Alpha focused on generating long-term outperformance through financial engineering. For a short time after launch, “The Quantamental Investor” will be offered at a heavily discounted legacy price. Stay tuned for more news!

Comments are closed.