lcva2

Thesis

Over the past 20 quarters, Microsoft (NASDAQ: MSFT) beat consensus analyst estimates — both in terms of revenue and earnings — 95% of the time. But arguably, few quarters have needed such an urgent pace as the upcoming Q1 FY 2023. After losing slightly less than 33% of equity value year-to-date, compared to a loss of around 25% for the S&P 500 (SPX), the feeling is very nervous for MSFT. Maybe down?

Looking for Alpha

In this article, I discuss everything an investor needs to know about Microsoft’s upcoming first-quarter fiscal 2023 results, which are due Oct. 25 before market.

Revenue overview

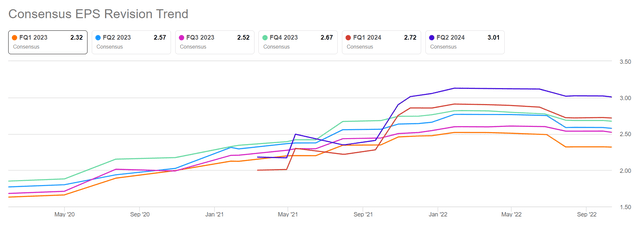

According to data compiled by Seeking Alpha, as of October 12, 33 analysts have submitted their estimates for Microsoft’s first-quarter fiscal 2023 results. Total sales are expected to be between $48.67 billion and $51.44 billion, with the average estimate being $49.82 billion. The dispersion is therefore quite wide. If an investor takes the average as an anchor, Microsoft’s first-quarter sales are expected to grow about 9.9% from the same quarter in 2021. EPS estimates range between $2.25 and 2. $46. The average is $2.32, which would imply year over year. growth of only 2.1%.

Regarding MSFT’s earnings forecast, investors should note two key points: First, the earnings forecast only estimates year-over-year EPS growth of just over 2% , which is clearly disappointing in my opinion. And second, earnings expectations (EPS revisions) for the third quarter are down more than 10% from the respective January 2022 expectations.

Looking for Alpha

Are the estimates too bearish?

Arguably, one of the main reasons why third quarter expectations are somewhat low is due to a very challenging macroeconomic environment – driven by inflation, rising interest rates, declining consumer confidence consumers and geopolitical tensions. And so, investors should note that whatever decline in the stock price is likely to be a function of the economy and not specific to Microsoft’s competitive moat, earnings growth and company profitability. company.

Smart Cloud – Loss of speed

To counter the negative impact of a slowdown, Microsoft has already announced slowing hiring, as well as potentially laying off existing employees. According to various news outlets, the downsizing primarily affects Microsoft’s cloud and security units.

This is surprising in my opinion, as the cloud – and in particular security – have been labeled as key growth areas for Microsoft. In fact, during the fourth quarter of fiscal 2022, management commented: (emphasis added)

In a dynamic environment, we saw strong demand, gained market share and increased customer engagement with our cloud platform. Commercial reservations increased 25% and Microsoft Cloud revenue reached $25 billion, up 28% year-over-year

Additionally, regarding security specifically, management told analysts:

As the rate and pace of threats continue to accelerate, safety is the top priority of every organization …

We take shares in all the major categories we serve. All up, our security revenue increased by 40% … We are the only cloud provider to protect all three major cloud platforms, and we see more and more customers turning to us to protect their multi-cloud and multi-platform infrastructure.

Has the environment changed so much since early June that the market is relying on outdated information? Maybe. Investors should consider how unexpected, fast-paced and vicious the environment has been for other blue chip companies such as Advanced Micro Devices (AMD), Amazon (AMZN) and Nike (NKE) – to say the least. name a few.

Reflecting on the above considerations, in my opinion, it is not unlikely that Microsoft’s main revenue driver – Intelligent Cloud, with around 45% of total sales – will disappoint in the first quarter of fiscal 2023.

personal computing

Microsoft’s personal computing division accounts for about a third of sales and includes Windows OEM products, Xbox content and services, search and news advertising, and Microsoft Surface.

The personal computing division already slowed in the fourth quarter of fiscal 2022, growing revenue only about 2% year-over-year to $14.4 billion. In addition, the September quarter marked a further slowdown in global PC demand – the biggest decline in demand in more than two decades.

Investors shouldn’t demand too much positivity here. But expectations are probably already very low.

Productivity and process

Reflecting on Microsoft’s September quarter, the key (open) question for me is “productivity and process” performance. A few months ago, Microsoft management commented that the segment is expected to grow between 12% and 14% in constant currency or $15.95 billion to $16.25 billion. And also added:

In Commercial Office, revenue growth will again be driven by Office 365 with seat growth across all customer segments and ARPU growth through E5. We expect Office 365 revenue growth to be approximately two points lower sequentially at constant currencies with a somewhat larger impact on US dollar growth than at the segment level.

While I understand that productivity gains and process optimization efforts must be essential for businesses in a tough economic environment, I doubt that businesses invest in these “optional” initiatives.

Personally, I think the lower estimate of the revenue guidance range ($15.95 billion) will be a more likely scenario.

other considerations

In Q4 2022, Microsoft returned $12.4 billion to shareholders in the form of share buybacks and dividends. But I think there could be a huge uptick in that number in Q1 2023 and/or in the future – given that Microsoft is a net creditor and generates about twice the cash flow from operations compared to which was distributed in fiscal year 4, 2022.

Microsoft’s business is firmly rooted in a subscription-based business model. As a result, the company’s revenue and cash flow are highly unlikely to fluctuate wildly from quarter to quarter. Note that in June 2023, Microsoft had approximately $43.5 billion in unearned revenue on the balance sheet.

Investors should consider that the risk may not relate to the last quarter of the first quarter of 2023, but the next quarters of the second quarter of 2023 and the third quarter of 2023, which could initially disappoint/surprise due to a weak market /strong. tips.

Conclusion

Heading into the September quarter earnings season, I’m less bullish on MSFT than I am on, for example, Meta (META) and Alphabet (GOOG) (GOOGL). I think Microsoft’s earnings estimate is reasonable – I just don’t think there will be a material upside surprise to sentiment.

Accordingly, I call the Microsoft stock a “Hold” entering earnings. But over the long term, I remain confident in the software giant’s earnings outlook. And there is no doubt that the company is undervalued.

Learn more about Microsoft: Is Microsoft Stock Cheap?

Comments are closed.