Jean-Luc Ichard/iStock Editorial via Getty Images

Microsoft (NASDAQ: MSFT) started 2022 on a slightly negative note, along with many tech stocks and the Nasdaq in general. The stock is currently at around 10% of its historical level high $350 and up analysts are already beating the table to use the decisive moment. We ask: “What defining moment?” Admittedly, Wedbush’s article wasn’t just focused on Microsoft, but it was the headline that garnered the most attention, as seen in the comment feed of the linked news article. We love action, but 10% on the back of a 500% run since 2017 doesn’t really sound like a bargain, let alone a defining moment.

In this article, we evaluate some positives and negatives and offer our sweet spot and an options strategy that we recommend using on the stocks you would like to own but at a cheaper price. Let’s start, with the negatives first.

No: history could repeat itself

Microsoft has been around so long at this point that it’s been called every name in the book when it comes to stock categorization. From being a start-up to a struggling company to a monstrous growth stock to a 15 year laggard back to a monstrous growth stock. Along the way, the company also became a 60% dividend aristocrat as it increased its annual dividend by 15 years.

Skeptics may argue that Microsoft spent 15 years going nowhere after the monstrous growth of the 1990s and there’s no guarantee that history won’t repeat itself after the recent growth spurt. In our view, this is unlikely, as the main reason Microsoft fell asleep soundly was the lack of a meaningful rival in the age of operating systems. In the age of the cloud and the metaverse, many other whales can eat Microsoft’s lunch at the slightest hint of complacency.

No: Possible multiple compression

Some of the biggest stocks of the past, including the former Microsoft and Cisco Systems (CSCO), have seen impressive earnings growth. What made returns (after the huge surges) anemic was the “multiple compression”, where earnings rose but expectations were so high that the market began to price the stock at a lower multiple. , which caused the stock price to stagnate or decline.

Forward estimates are usually compiled based on the next year’s earnings estimates. Mr. Market is usually not too patient. But considering Microsoft’s recent run and how good it is, let’s see what the multiple before [PE] is based on fiscal year 2024 earnings estimate. With expected earnings per share of $11.93, Microsoft is trading at a multiple of nearly 27 based on fiscal year 2024 estimates. could happen by 2024 and that multiple doesn’t seem cheap. Of course, on a hand-picked basis of comparison, it might seem cheaper, but we won’t be surprised by either (or both) of these two scenarios: high revenue expectations turn out to be too high or the market does not attribute high multiples, even to a recent winner like Microsoft.

(Source: Search Alpha)

Yay: Metavers

Yes, you read that right. Microsoft is not one of the two names that comes to mind when talking about Metaverse. This distinction belongs to Meta Platforms (FB) and Nvidia (NVDA). But Microsoft’s foray into Metaverse only makes sense given its presence in our daily lives, especially its official side. Microsoft Teams is a collaborative tool that has become more famous day by day since the onset of the COVID pandemic. Microsoft is taking Teams to the next level by introducing “Mesh”, which it says will be the gateway to Metaverse. Mesh will introduce Avatars to make meetings more personalized and “to take their avatars to immersive spaces to experience these fortuitous encounters that spark innovationClick here for more on this in Microsoft’s own words.

This article by SA author Jonathan Weber argues that Microsoft taking Metaverse seriously will add spark to its actions.

(Source: News.Microsoft.Com)

Yay: quality wins

Whenever the tech sell-off stalls and market makers decide to buy tech stocks and ETFs, Microsoft will rightfully be one of the first names to grab attention.

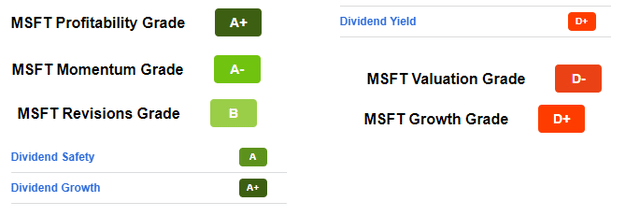

Seeking Alpha’s quantitative ratings offer confirmation of the stock’s high quality in many aspects, including profitability, momentum and dividends, as shown below. Naturally, the yield gets a D+ as the monstrous rise in the stock price has reduced the yield. But keep in mind that Microsoft has increased its dividend every year since 2006, and the stock’s five-year dividend growth rate is an impressive 9.40%. In other words, the poor performance is not because the company cannot or does not increase its dividends, but because the stock price exceeded expectations.

The D- valuation rating is also unsurprising, as the market has been looking for high-growth names over the past couple of years. We think the stock has even more downside here and could hit $200 (say $280 to $290) before bouncing back.

A growth rating of D+ is a bit of a concern, but looking at the details here, the three important metrics of growth: revenue, EPS, and free cash flow are all well ahead of the industry. However, given the increased valuation and general earnings optimism, a multiple squeeze would be natural should earnings rise.

(Source: Search Alpha)

Other Ways to Buy: Consider Selling Put Options

If you want to acquire Microsoft but at a lower price, selling may be your best ally. Options are generally considered risky and complicated by many long-term investors. However, once the risks are understood, options can go hand in hand with fundamental and long-term investing. Hard to believe? Even the god of “Buy and Hold” investing, Warren Buffett, has used this strategy successfully.

Consider selling put options only under these conditions (all three must be met):

- The underlying stock is something you would like to own, if attributed to you.

- The strike price is something you are comfortable with.

- Your put options are cash secured, which means you have enough money to buy the underlying stock if your strike price is reached on the expiration date.

Thank you readers of our previous article on selling put options, please beware of company-specific known events like the ones below before selling a put option:

- Next ex-dividend date before the put option expires, as the amount of the dividend deducted from the stock price brings the stock closer to the strike price of the option. Microsoft will have two Ex-dividend events between now and the options chain expiration date which we explain below. But given the low yield (62 cents on a $314 stock), the quarterly dividend deducted from the stock shouldn’t have too much of an impact in this case.

- Next earnings release near option expiration date as volatility increases. Microsoft will release two quarterly results during this period.

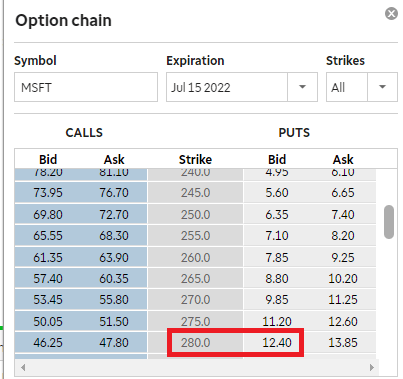

Below is a put we rate on Microsoft. To explain this in simple terms, we need to set aside $28,000 to be able to buy 100 Microsoft shares at a strike price of $280. Mr. Market is willing to pay us a premium of $1,240 for this. This is a return of 4.50% in 6 months on the $28,000 that we must set aside for this contract. Generally, we prefer options that expire in a month or two, but we strongly believe Microsoft’s rocky start to the year isn’t over yet.

Returning to this example,

- If Microsoft trades above $280 when the option expires on July 15, 2022, that put option will expire worthless and we will retain the premium of 4.50%, more than 5 times the stock’s current yield.

- If Microsoft were trading below $280 when the option expires on July 15, 2022, we would be forced to buy 100 shares at $280, regardless of the market price at that time. However, with the perceived premium, our breakeven price for this trade is $267.60 ($28,000 minus $1,240 divided by 100 shares).

- There is also a third way to close this options chain and that is called “Buy to Close” where if we think we have obtained a significant portion of the premium we will close the position before July 15, 2022 and repeat the process at a different expiry/strike price combination.

(Source: TDMeritrade.com)

Why are we considering the $280 price range?

At this point, you might be wondering why we used the $280 price range a few times in the article. Here is.

- $280-$290 would be our preferred entry point from a technical standpoint, as this represents the stock’s 200-day moving average.

- $280 represents a 20% sell off from the all-time high of around $350. A 20% selloff is considered a bear market and strong stocks like Microsoft are unlikely to stay in this region long, if at all, they will get there in the first place.

- $280 is also more than a 10% drop from the current stock price, providing a relative margin of safety.

Conclusion

To repeat the cliché, price is what you pay and value is what you get. We certainly see the value in Microsoft, the company. But the price is not yet in our alley. We continue to hold our existing shares (including dripping dividends) and will add shares in the event of significant withdrawals. Until that event, selling puts gives us some middle ground to stay in the names we love while not missing out on the game entirely.

Comments are closed.