Wachiwit/iStock Editorial via Getty Images

Microsoft Corporation (NASDAQ: MSFT) is a fundamentally sound company and continues to grow rapidly despite its massive size. Although the technology sector has recently suffered significant losses and supply chain issues continue to cause problems, Microsoft continues to innovate and plans to release new products and additions to Edge. However, the company’s shares may be overvalued and are poised for a sharp pullback.

Microsoft has exceptional fundamentals and continues to grow

Microsoft has very few flaws with its fundamentals and continues to grow rapidly, despite already being worth around $2 trillion. The company is able to generate revenue and profit efficiently, manage its assets well and manage its liquidity effectively.

Revenues and profits continue to grow

Over the past 5 years, Microsoft has been able to increase its revenue from $96.57 billion to approximately $168.09 billion, calculating an average annual growth rate of 14.87%. The gross margin is even more impressive, standing at around 66.48%. The profit margin declines from here, but remains an impressive 28%. This decrease stems from high SG&A and R&D costs, both amounting to around $20 billion each.

It is important to mention the 3 major segments of the business. The first is More Personal Computing and includes Windows, Xbox, etc. This segment represents approximately 32.2% of sales. The next segment is productivity and business processes and is mostly made up of office. This segment represents 32.1% of sales. The last segment is Intelligent Cloud and includes server and Azure products. This segment is growing rapidly and represents around 35.7% of turnover.

In the company’s latest earnings report, Intelligent Cloud impressed investors. This segment was able to massively increase its revenue, with Azure and other cloud services standing out growing by 46%. Overall, the company’s income statement is in excellent health.

A strong balance sheet gives an excellent cushion

Microsoft’s balance sheet tells the same story as its income statement. The company has a current ratio of 2.0 and its current assets are mostly comprised of cash of approximately $104.69 billion. It is also important to mention the $32.61 billion in receivables.

As for the debt, it may seem high at first glance at $64.47 billion. However, the net debt is significant and stands at -26.68 billion dollars. This gives Microsoft a Net Debt/EBITDA ratio of -0.3, demonstrating sound debt management.

With many investors predicting a recession is imminent, Microsoft’s strong balance sheet can help it protect against economic problems and continue to innovate and create new products.

Impressive cash flow and stock buybacks

Over the past 5 years, Microsoft was able to nearly double its operating cash flow from $39.51 billion to $76.74 billion. This is mainly due to its high net income as a starting line combined with a consistently high added depreciation. The company’s capital expenditures are also increasing, but remain low relative to operating cash flow. Over the past 5 years, the company’s investments have grown from $8.13 billion to $20.62 billion.

Microsoft is also withdrawing stock and debt, but is much more focused on stocks. In the company’s latest report, $8.35 billion in stock was withdrawn, along with $4.2 billion in debt. This allows investors to see increased value in their investment, as well as a good way to use the company’s huge cash reserve.

The tech sector is struggling and not improving

The technology sector has suffered significant losses recently and shows no signs of improvement. The Nasdaq is down about 25% year-to-date, and the big players are down even more. Companies like Zoom (ZM) and Spotify (SPOT) have fallen over 60% in the past 6 months, and even Netflix (NFLX) has fallen over 70%.

A big problem that culminates in the sector is the problem of overstaffing. Recently, Meta (FB) said the company will cut hiring due to lower revenue caused by Apple’s (AAPL) privacy changes. Amazon (AMZN) continued on this theme saying the company is overstaffed. Additionally, companies that have thrived during the pandemic, such as Zoom and Robinhood (HOOD), will likely have to cut back on hiring as demand for their products now declines as the pandemic subsides. In fact, Robinhood has already laid off around 9% of its workforce.

Given that many tech companies are massively overvalued, an even bigger correction could occur. A good example is Tesla (TSLA), which is worth more than 6 times the combined value of Ford (F) and General Motors (GM) combined. If things don’t start to look up for the sector, tech companies (including Microsoft) could suffer even bigger losses than they currently do.

Xbox TV and Edge additions could lead to increased revenue

Microsoft does a great job of innovating and creating new products. It was recently revealed that the company plans to launch a new product, Xbox TV, in 2023. This product will be a competitor to Amazon Fire Stick and Roku Streaming Stick (ROKU). However, this product has a unique advantage over its competitors. Not only can an individual watch shows and movies with the apps on the device, but they can also play games using Xbox Game Pass Ultimate. To further strengthen the product, Microsoft is partnering with Samsung (OTC:SSNLF) to help develop streaming apps on the device, allowing Samsung Smart TV owners to use the app without having to purchase the device.

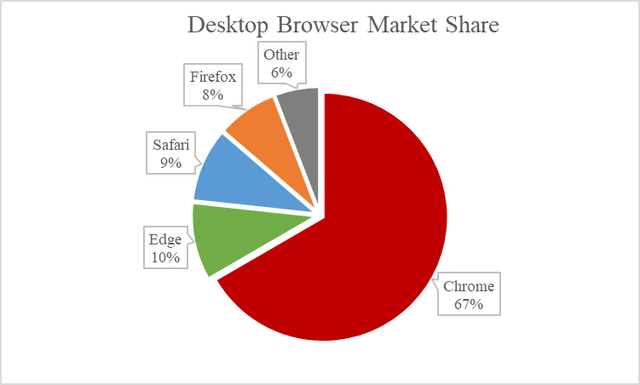

Another product extension is the addition of a free built-in VPN for Edge. Recently, Edge overtook Safari to become the second most used desktop browser in the world, just behind Google Chrome (GOOG).

Global desktop browser market share (GlobalStats, chart by author)

This free VPN is an effort to make Edge more popular with users and eat away at Google’s huge market share. Opera is the only other browser with a similar free VPN. While Firefox and Chrome have VPNs, they have to be paid for.

Supply chain issues are still relevant

Supply chain issues continue to be a recurring theme in the market. China’s zero-tolerance policy may cause factory shutdowns and further exacerbate chip shortages. This shortage of chips caused problems with PC and Xbox production and harmed the company’s More Personal Computer segment. That being said, it’s important to note that not all segments of Microsoft are chip-based. The Business Productivity and Processes and Intelligent Cloud segments are not heavily dependent on chip production, which means they are quite resilient to supply chain issues. With these two segments accounting for approximately 67.8% of revenue, combined with the previously mentioned fact that the Intelligent Cloud segment is growing rapidly, one could conclude that more serious supply chain issues may not be detrimental to Microsoft.

Evaluation

Microsoft’s stock valuation is one of the only downsides to the company. When calculating a DCF of the company with its WACC of around 9.37% as the discount rate, a fair value of around $172.93 per share can be found. This means that Microsoft’s stock could be overvalued by around 34.64%.

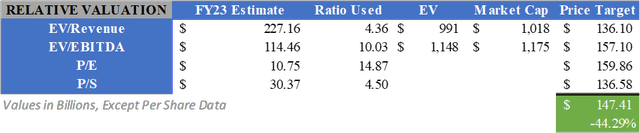

A relative valuation does not indicate better signs. Using FY23 estimates for revenue, EBITDA and earnings and combining them with industry median ratios, a fair value of $147.41 can be calculated. This would mean that the stock is overvalued by around 44.29%. No matter how you look at it, it’s clear that Microsoft (along with the tech industry as a whole) is currently heavily overvalued.

Microsoft relative rating (created by author)

What should investors do?

While Microsoft is a fundamentally excellent company and can fairly defend itself against current tech industry issues and supply chain disruptions, the company’s stock value may be too overvalued for some to handle. If banks forecast that a recession is approaching and stocks pull back even further, Microsoft could see huge declines in the stock price, but with little effect on the underlying business. This leads me to believe that it might be best to wait until Microsoft’s stock price drops before buying, and apply a hold rating for now.

Comments are closed.