lcva2

Microsoft Corporation (NASDAQ: MSFT) just announced its annual dividend increase, as Seeking Alpha covered here. The new quarterly dividend of 68 cents per share represents nearly 10% dividend growth and marks the 13th consecutive year that Microsoft has announced a dividend increase in September.

Why is the month important, you may ask, as annual dividends increase year on year. We offer two reasons: (1) reliability on the part of the company; and (2) the ability to plan for reliability for income-seeking investors. Even those who cast a shadow over dividend growth stocks due to inflation may not have much to say about a double-digit increase.

Microsoft and even the world as a whole, you might say, have changed a lot since that article we wrote in 2014. But the fundamentals of investing in dividend growth haven’t changed. Therefore, this article uses the same model and compares how things look now versus eight years ago. Let’s start.

New Yield: New annual dividend of $2.72/share gives Microsoft a yield of 1.12%. That’s much less than the 2.66% after the 2014 dividend increase. No price to find the reason, though: the stock price has since increased almost 6 times, from $47 to $242. Even dividend enthusiasts wouldn’t complain about this price change, as Microsoft was stuck in a tight trading range for nearly a decade before breaking out thanks to its Azure dominance.

The payout ratio: Here is the kicker. Despite 8 more years of dividend increases since the 2014 article, Microsoft’s current term payout stands at 26% compared to his 46% in 2014. Add to that the stock price increase mentioned above, and you can clearly see the health of Microsoft’s earnings and the potential for dividend growth.

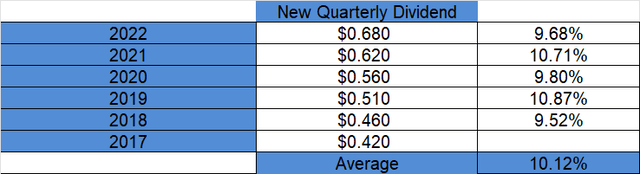

Dividend Growth Rate (DGR): At the time of our 2014 article, Microsoft’s 5-year dividend growth rate ranged between 10% and 25%. In contrast, the recent five-year range is much narrower between 9.52% and 10.87%. Why are we optimistic about this? This shows a more mature and reliable company when it comes to its dividends. To use a parallel with the world of running, runners enjoy what are called “tight gaps” for each mile, where the range of results is more predictable and leads to long-term success.

MSFT DG (Seeking Alpha)

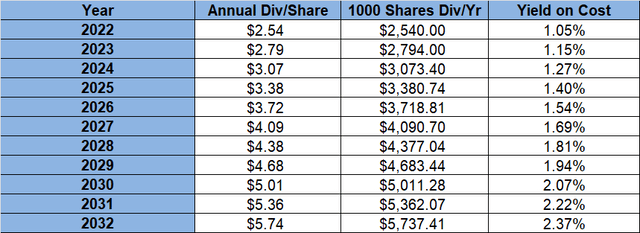

Extrapolation: To keep things consistent with the 2014 article, the table below assumes dividend growth of 10%/yr for the next 5 years and 7%/yr for years 6-10. This seems very cautious given the distribution margin, plus the expected double-digit earnings growth rate. It’s easy to scoff at this figure, but keep in mind that if the company realizes that it cannot use its profits and capital more productively, it will most likely increase the payout ratio. This means that the total return for investors should still be satisfactory given the combination of earnings growth and dividend growth.

MSFT DG Expectations (Author)

Forward thinking

- A stock trading at the bottom of its 52-week trading range alone does not make it a buy. However, it offers a compelling story if the company’s fundamentals don’t deteriorate. No one can seriously say that Microsoft, the company, won’t be around for the next few years. Microsoft, the stock, has been inflated like almost every other stock in the market, but after falling from $350 to $240, Microsoft is trading at a multiple of 24. If you think that’s excessive, Procter & Gamble (PG) is trading at 23 and our beloved Coca-Cola (KO) is trading at 24. When inflation, unfortunate war, COVID and other macroeconomic conditions stabilize (they don’t even need to improve), stocks like Microsoft will catch early bids.

- You’re not to blame if you’re fed up with cloud growth stories. It has to stop at some point, you think. You may be right. But that point isn’t coming soon, as Microsoft’s Azure still shows sequential strength whether you look at it quarterly or yearly. The company recently announced that it also expects double-digit growth in the coming quarters. It’s kind of funny and gratifying to read what we wrote in the 2014 article about Microsoft’s cloud potential: “The company emphasizes Cloud and Enterprise Mobility Suite. While Microsoft’s phone didn’t change the world, even Apple (AAPL) fans have to admit that the Cortana vs. Siri ad is hilarious and straight to the point. If consumers get your message right, chances are your products will recover as well. Windows tablets could have a nice run according to this article on Seeking Alpha. Long story short, there are encouraging signs that Microsoft could be more than just a dividend stock.”

- If earnings grow 15% per year as expected, earnings per share will be $20 in 5 years. Even if the payout ratio remains at the current low level of 26%, that would give investors an annual dividend of $5.29 per share. This would be almost double the current $2.72/share. Not too bad.

Conclusion

We have all been envious at some point in our lives. We believe that others have everything one way or another: money, fame, health and beauty. In the investment world, the 4 cornerstones according to us are stability, capital appreciation, dividends and balance sheet strength. Few companies have it quite like Microsoft. We remain loyal to Mr. Softie throughout this sale and appreciate the “SWAN” (sleep well at night) attribute he brings to our portfolio.

Comments are closed.