cold snowstorm

Introduction

There’s not much to like about tech stocks, as most companies report disappointing numbers and provide disappointing guidance that forces analysts to cut estimates in the blink of an eye. While the software space has certainly benefited from the pandemic tailwinds and is does not escape a reversion to the mean, Microsoft Corporation (NASDAQ: MSFT) is a solid name that deserves our attention as macro pressures continue to drive down tech valuations.

Back to the case of the bull

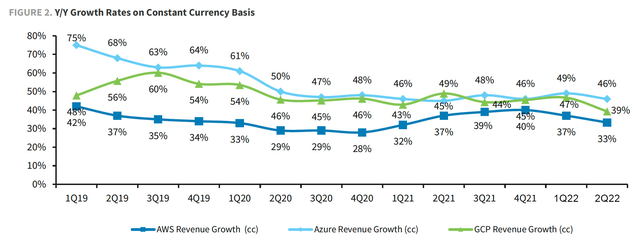

The simplest bull case for Microsoft is that the cloud migration remains a sustainable growth story despite some moderation. From a top-down perspective, the 1S22 was strong for the public cloud market, which saw over 35% growth, although the big three (AWS, Azure, GCP) saw some deceleration on compositions more difficult. The top three cloud providers now have a total annualized run rate of $147 billion, which was up 36% year-over-year in Q2 from 41% in Q1.

Azure is estimated to have a gross margin of over 60%, while AWS (AMZN) reported an operating margin of 29% in the second quarter. Google Cloud Platform (GOOG, GOOGL), the third-largest remote provider with less than 10% market share, has yet to make a profit but still delivered 36% YoY growth in Q2 vs. 44% in Q2. T1. Unlike some pockets of the tech sector that have been one-time beneficiaries of the pandemic, there is no doubt that cloud migration will continue to be a structural rather than a cyclical theme.

Company data, Barclays

Azure outlook remains strong

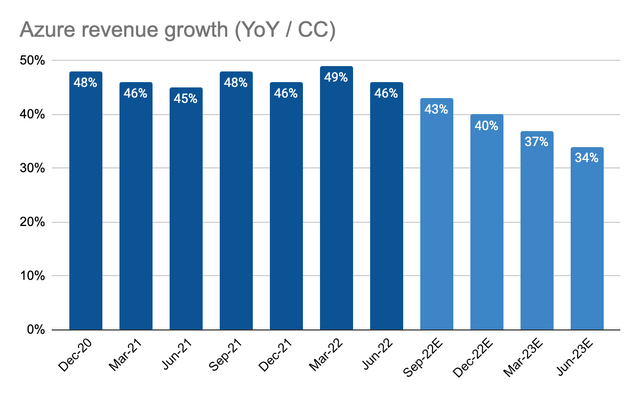

In the June quarter (4QFY22), Microsoft reported total revenue growth of 12.5% YoY and +16% in constant currency, which was roughly in line with consensus. Despite some currency impact from a strong dollar, total RPO increased 32% from 28% in the prior quarter. Commercial bookings increased 37% CC to $189 billion. Management highlighted a record number of Azure transactions above $100 million and $1 billion. Azure sales increased 46% (1% below consensus) and are expected to increase 43% in the September quarter (1% below consensus). Despite the slight moderation amid macro concerns over more consumer-centric industries and SMEs, Azure’s growth remains strong on longer booking commitments.

While CEO Nadella was cautious about macro developments during the earnings call, he viewed cloud transformation as a deflationary force in an inflationary environment where companies are forced to do more with less.

That’s why I think that coming out of this macroeconomic crisis, the public cloud will be even more of a winner because it acts as a deflationary force. – MSFT call 4QFY22.

Besides Azure, demand for cloud security continues to be favorable as enterprises look to spend more to protect their data and digital operations. Microsoft reported security revenue growth of 40% year-over-year, approaching the $20 billion mark.

For the September quarter (1QFY23), Azure’s growth is guided to decelerate from 46% CC to 43% CC, where management highlighted some weakness in consumption. Assuming growth slows by about 3 points per quarter going forward, Azure could exit FY23 with a still respectable 34% growth rate in Q4. As the current macro story puts pressure on the technology as a whole, Azure is in an enviable position to capitalize on a strong IaaS (Infrastructure as a Service) market that is expected to grow another 30% to $156 billion in 2023 (Gartner).

Company, Albert Lin

PC smoothness is a problem, but a well-understood problem

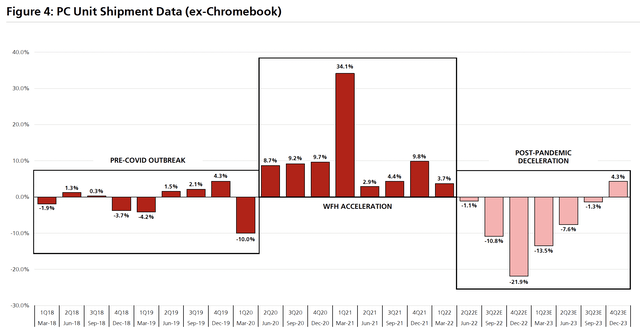

Microsoft’s Office and Windows revenues are certainly not immune to a slowdown in the PC market. Since the PC segment has been one of the main beneficiaries of the pandemic, all PC manufacturers have seen a normalization in demand this year:

- Asus: With demand headwinds, many are looking at a 10-15% decline in the PC market in 2022.

- Lenovo: The PC market is experiencing weak consumer demand and supply chain issues due to Covid-19.

- HP: Weaker consumer demand and increased price competition

- Dell: Demand has slowed, B2B customers are delaying purchases and are more conservative on IT budgets.

Gartner, UBS

Although the weakness in the PC market will put pressure on Office and Windows revenues, the Windows operating system remains in the dominant position while Office products are very sticky. Microsoft has implemented a 15-25% price increase across the Office family of products, which is a clear indication of pricing power, a highly desirable attribute in an inflationary environment. Overall, while the PC business is undoubtedly experiencing a post-Covid-19 slowdown, markets should already have priced in the impact because nothing lasts forever.

Recent decline presents another buying opportunity

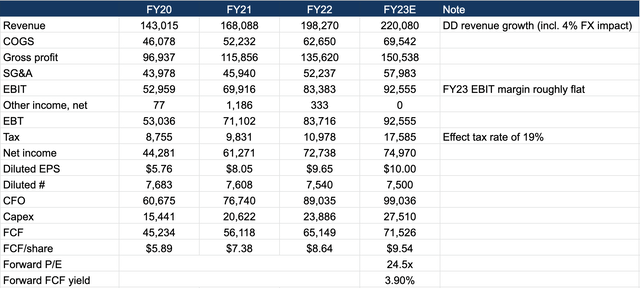

Microsoft’s FY23 forecast calls for double-digit revenue growth with a 4% impact from FX. This shows the relatively robust and defensive nature of the company’s offerings, which should reduce downside risks in my view. While operating margins are expected to be stable (favorable impact of the amortization plan offset by exchange rates), the estimated operating margin for FY23 of around 42% and the FCF margin of around 33% make always from Microsoft a source of profit.

While Microsoft’s valuation isn’t exactly in bargain territory, I suspect negative investor sentiment and cautious positioning should be a good setup for better-than-expected results going forward. As a result, I view the recent share price decline as a buying opportunity at 24.5x forward earnings / 3.9% forward FCF yield and will start to get more aggressive if the valuation breaks the decline at ~ 20x or ~$200 per share.

Company data, Albert Lin

Comments are closed.